Mortgage Delinquencies: What does it mean for NHC

Mortgage delinquencies are spiraling upwards around the world due to the Covid-19 pandemic, thus leaving a further strain on the financers and our economic systems. One can assume that we, globally, will experience a market crash at some point.

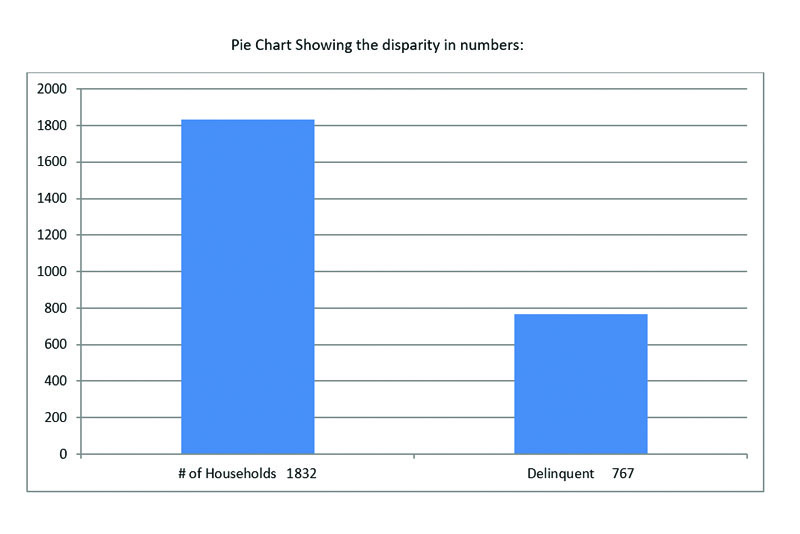

At NHC, mortgage delinquencies have been climbing pre-Covid-19. Overall, the rate of delinquencies is just over 40%, which is a large percentage when compared to the loan portfolio. The spike in delinquency during the pandemic was the biggest rise in the history of NHC.

Despite the government’s Stimulus package and other poverty alleviation strategies, mortgage payments seem to be the least of homeowners’ priorities.

How do we justify people not paying their mortgage, pandemic or no pandemic? Persons who are qualified for a home mortgage through NHC are “usually” considered persons who are in a lower income bracket. Hence, their interest on the loan will range from 2% to 5%, the down payment is minimal to nothing at all with a repayment period of 30 years that provides for a very low monthly payment. So, to answer the question above, the answer is simple; there is no justification for not paying your mortgage, at NHC that is. In fact, one should be eager to make their payments as opportunities such as these are very rare.

What will happen to NHC should the delinquency keeps increasing? NHC has made and continues to make it easier for homeowners. The Client Relations’ staff contacts the homeowners via various medium to offer them a refinancing option. There is also a moratorium provided for persons who have lost their jobs due to the pandemic. Quite a number of homeowners are apprehensive and have not taken advantage of these offers. As such, if the number of delinquent households continues to rise it only means that at NHC, the demand will be more than the supply. This can be detrimental for many families as staff can be sent home, homes will be foreclosed, opportunities to get a loan and a VISA to travel will be denied and families who really need a home will not have that opportunity through NHC. It can also lead to the garnishing of homeowners’ PAP allowances.

How can this be reversed? Homeowners have to be responsible and abide by the commitment that they made. Speaking with a Client Relations’ Officer to refinance the mortgage will get you out of a delinquency status and give you a better credit rating.

NHC is a subsidiary of the Government of St. Kitts and Nevis and is supported by the Minister of Human Settlement et al, the Hon. Eugene Hamilton, along with the Board of Directors.